[Disclaimer: I am not an accountant nor am I qualified to provide tax advice. You should seek professional advice before taking action on any of the ideas presented here.]

For those looking to invest in marketplace lending or any fixed income investment there is a strong case for doing so within a tax advantaged account. To better understand the reason for this it’s important to realize that income from loans invested with LendingClub or Prosper is taxed at ordinary income tax rates. This means that you will be taxed at the same rate as you would if you currently earn wages as a W2 employee.

Tax rates for 2018 start at 10% and go up to 37% for the highest wage earners. It’s important to understand how this ordinary income affects taxes compared to other asset classes like equities. Generally speaking when investing in stocks, investors are seeking the long term appreciation of assets or dividend income. As an example, the S&P 500 ETF (Ticker: SPY) which tracks the largest public companies has a 12 month yield of around 1.70%, lower than a typical marketplace lending portfolio. Depending on your tax bracket both long term capital gains and dividend income may be taxed at lower rates than ordinary income. For further understanding of tax implications you can look at the tax rate tables of ordinary income and capital gains.

Marketplace lending is unique in that you will almost always have short and long term capital losses. This is because you are bound to have defaults in your portfolio (unless you have a small account AND are extremely lucky). Let’s assume you decide to invest through a taxable LendingClub account. In a given tax year, you are only allowed to deduct $3,000 in losses against your ordinary income unless you have capital gains to offset the losses. Note that this is on the federal level and your state may have different guidelines.

If you have a sizable investment in LendingClub and have no capital gains you’ll have to carry forward any losses beyond the $3,000 to future years. Thus, you are losing out on the ability to deduct some losses in the year you incurred them (assuming your losses surpass $3,000). This drag becomes more significant the larger your account. This is why investing in an IRA account is so appealing for marketplace lending investors. You are not taxed on any income earned from the loans so deducting losses becomes irrelevant.

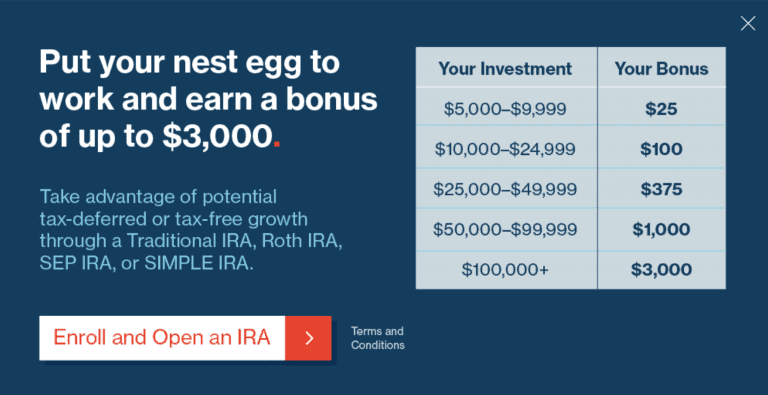

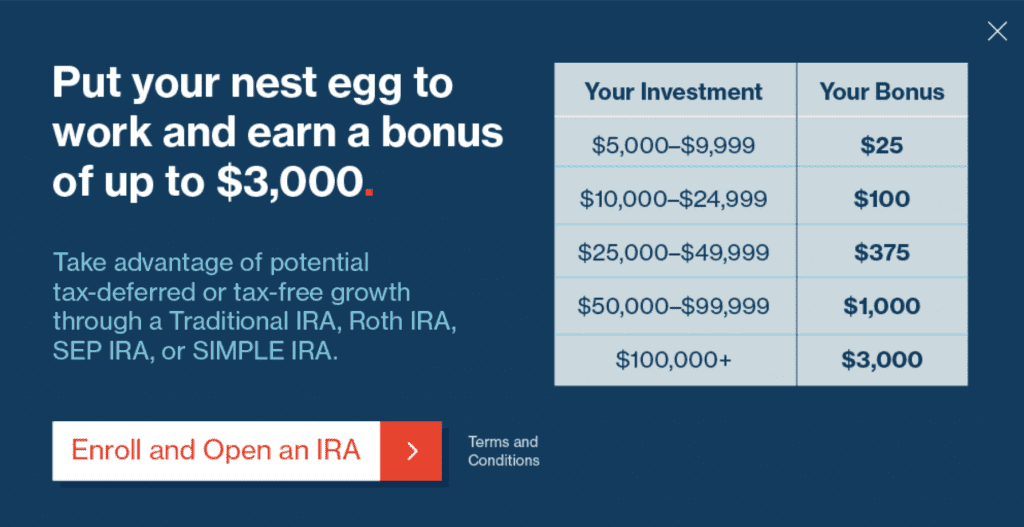

LendingClub Offering a Bonus for IRA Investors

After understanding the benefits of investing through an IRA it’s worth mentioning that LendingClub offers bonuses for new accounts. The bonuses range from $25 all of the way up to $3,000 and are available on Traditional IRAs, Roth IRAs, SEP IRAs or SIMPLE IRAs. Below are the bonus amounts in place for 2018.

When you setup your IRA account you’ll need to work with a custodian. LendingClub now has a new preferred custodian called IRA Services or ISTC for short. ISTC charges an annual service fee, but this fee is waived provided your account maintains a minimum invested balance of $5,500 in LendingClub Notes.

Conclusion

For investors looking to allocate to LendingClub it is worth considering investing through an IRA. While we’ve presented an overview of the benefits and some details as to why it might make sense from a tax perspective it’s important to understand any tax implications for your specific situation. Remember that you have until April 17, 2018 to contribute to a Roth or Traditional IRA for the 2017 tax year.

If you’re looking to open a LendingClub account, you can do so using our affiliate link.