Europe·Feb. 3, 2023Zopa bank raises $92 million for possible M&AFintech funding rounds of this size are few and far between- Zopa plans to use the investment to further its plan to "be Britain's best bank." Read Full Story

News Roundup·Sep. 21, 2020Digital Banks Hit Bump in the Road, But Pandemic Has Silver Lining[Editor’s note: This is a guest post from Ryan Weeks, formerly with Dow Jones and AltFi, covering fintech. This is... Read Full Story

Asia/PacEuropeFintechNews RoundupUSA·Jul. 29, 2020More News for July 29, 2020Cboe Proposes Plan That Could Curb Advantages of Fast Traders European banking needs a Big Bang Hong Kong-based EMQ raises... Read Full Story

EuropeFintech·Jul. 24, 2020Where are the Founders from Some of the UK’s Top FintechsAltFi has taken a look at where the founders from some of the top UK fintech companies went after leaving... Read Full Story

EuropeUSA·Jul. 16, 2020Morningstar predicts ‘positive year’ for European securitizations despite pandemicWhile leaving wide open the question of “what happens as we head into the summer and fourth quarter of 2020,”... Read Full Story

Fintech·Nov. 30, 2022Cost of living crisis critical: UK fintech sector mobilizesWorsening conditions for the public's financial health have caused the FCA to launch a consultation. The fintech sector is already way ahead. Read Full Story

EuropeFintechUSA·Aug. 5, 2020More News for August 5th, 2020Mobile bank Current launches a points rewards program for debit card users U.S. Financial Service Buckle Secured $31 Million Through... Read Full Story

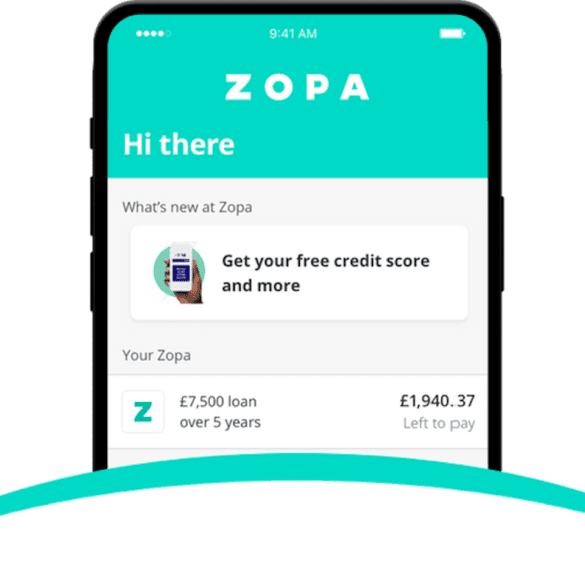

EuropeFintech·Jul. 28, 2020Zopa Announces Interest Rates on Savings ProductsHot on the heels of their banking license approval last month, leading UK fintech Zopa has announced interest rates for... Read Full Story

Asia/PacEuropeFintechNews RoundupUSA·Jul. 17, 2020More News for July 17, 2020Clearbanc just launched a valuation tool that its cofounders are calling a credit score for startups. Here’s what entrepreneurs need... Read Full Story

EuropeFintech·Jul. 15, 2020Peer-to-peer lending at an inflection pointZopa CEO Jaidev Janardana is bracing for a “moment of truth” for the peer-to-peer lending industry, which Zopa has led... Read Full Story