Opinion·Jun. 9, 2021Three things Policymakers can do to help American small businesses after the Paycheck Protection Program[Editor’s note: This is a guest post from Ryan Metcalf, Head of Public Policy & Social Impact at Funding Circle.] The Paycheck... Read Full Story

Lending·Jan. 11, 2021Fintech Lenders and Banks Are Ready for PPP Round TwoThe second (third?) round of the Paycheck Protection Program kicked off today and it was very different to when the... Read Full Story

News Roundup·Nov. 23, 2020PPP Loan Forgiveness: The Next Role on the Fintech Stage[Editor’s note: This is a guest post from Susan Doktor. She is a journalist and business strategist who hails from... Read Full Story

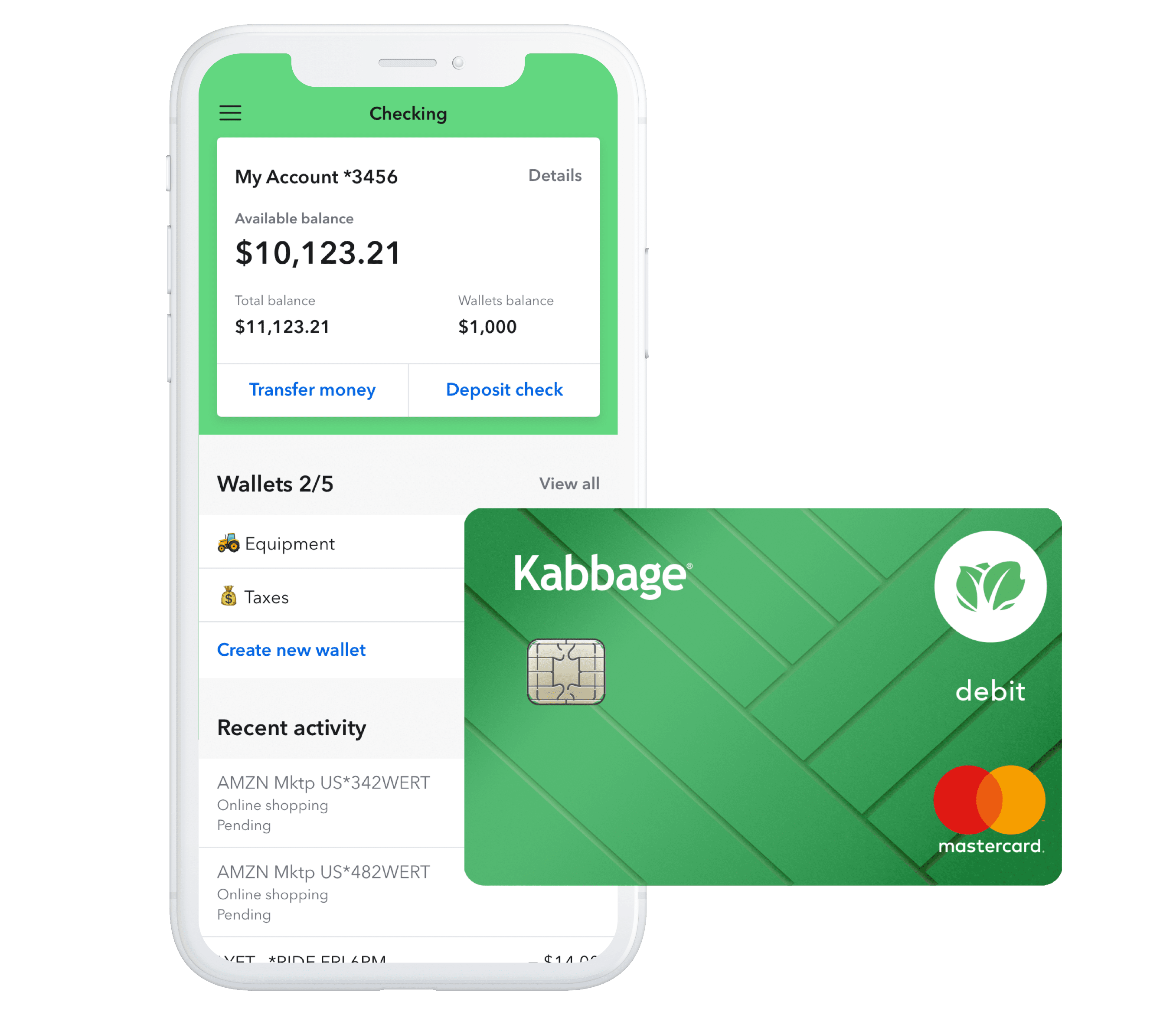

FintechUSA·Jul. 22, 2020Kabbage Launches Checking Accounts for Small BusinessToday, Kabbage announced the launch of their new small business checking account called Kabbage Checking; it is being offered in... Read Full Story

News Roundup·Jul. 22, 2020Kabbage Launches Checking Accounts for Small BusinessMany (perhaps most) small businesses are not well served by their bank. This was made clear during the Paycheck Protection... Read Full Story

Guest PostLendingRegulation·Mar. 8, 2021Fintechs Saved PPP and Should Be Included in the State Small Business Credit Initiative[Editor’s note: This is a guest post from Ryan Metcalf, Head of Public Policy & Social Impact at Funding Circle.] Fintech... Read Full Story

News Roundup·Dec. 22, 2020The PPP is Back, What do Fintech Leaders Think?Last night Congress finally passed a new round of stimulus funding. The $900 billion Covid-19 relief package included $285 billion... Read Full Story

FintechUSA·Aug. 3, 2020Brock Blake on Whether PPP Loans Should Be ForgivenWriting in Forbes, the CEO of Lendio, Brock Blake, argues that small business loans obtained through the Paycheck Protection Program... Read Full Story

Asia/PacEuropeFintechNews RoundupUSA·Jul. 22, 2020More News for July 22, 2020Congress wants to extend PPP, lenders ready to move on Groundfloor Says Q2 was a Record Quarter Broadhaven Ventures’ Michael... Read Full Story

FintechUSA·Jul. 20, 2020Lend Academy Podcast: Lexi Reese of GustoThe COO of cloud-based payroll and benefits provider, Gusto, discusses how they were able to pivot so quickly to offer... Read Full Story