Green Dot Eyes Banking-As-A-Service, Gen Z To Build On Q4 Growth $650 billion asset manager Franklin Templeton is embedding data...

This week saw three fintech firms representing payments, debit, and credit post results. Although each saw momentous growth year over year, in some cases, it was not enough to outpace expectations after this bull run of a year for fintech.

Green Dot’s Founders & CEO Steve Streit left the company in December 2019 as they were transitioning from prepaid card...

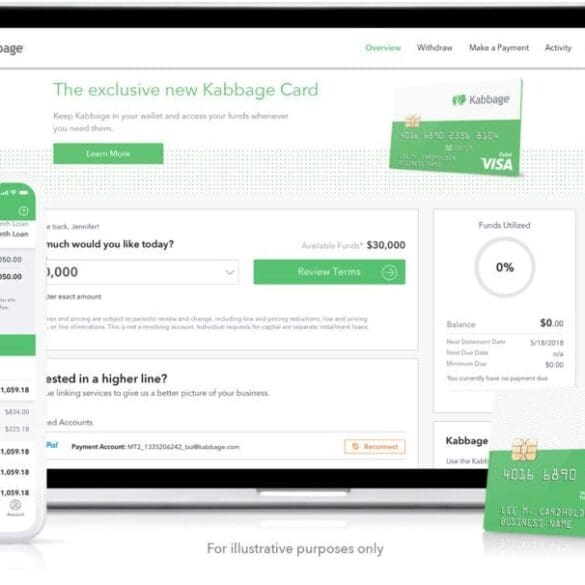

Today, Kabbage announced the launch of their new small business checking account called Kabbage Checking; it is being offered in...

Remittance fintech Pangea is launching a bank account tied to their current product due to user based feedback; “It was...

Kaspersky Lab Sees Spike In Mobile Banking Cyberattacks Zero raises $20 million from NEA and others for a credit card...

Green Dot is planning to launch a new affinity banking service called Bank OS, this would be a simpler version...

The fintech world is not taking the summer off. New developments are coming fast and furious, from fundraisings to product launches to government intervention.

Banking for brands startup Bond raised $32 million to capitalize on the exploding trend of B2B2C banking.

Samsung Money launched, leveraging SoFi’s infrastructure. As SoFi again seeks a national banking charter, they could become the de facto leader in this space.

Kabbage and Intuit launched small business bank accounts as extensions of their already deep relationships with SMBs.

And WhatsApp is trialing all sorts of financial services in India just as Chinese fintech super apps are being banned from the country.

Embedded finance can help small businesses manage their money end-to-end, but not all companies are equipped to offer it properly.

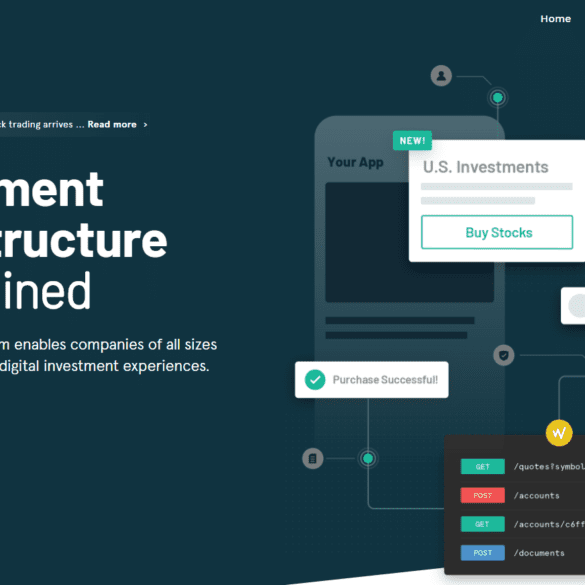

I look at two mental models explaining why and how financial APIs have led to the creation of billions in enterprise value. The driving news is that Square Cash is competing with Robinhood in free trading, powered by trading API company DriveWealth. Last week, we saw that Chime, Robinhood, and Monzo were powered by payments API company Galileo. Should these enablers be worth the billion-dollar valuations of their clients? Are APIs inevitable technology progress? Or are we just seeing venture financing spilling desperately into a rebundling play to find profitability?