American Banker reports on the lobbying group called Financial Innovation Now and that some technology giants are meeting individually with government agencies; Amazon met with the OCC starting in the second quarter of 2016 and met again this year; PayPal has also met with OCC officials in several quarters last year. Source

When I started LendIt with my fellow co-founders back in 2013 I was most excited about how online lending could...

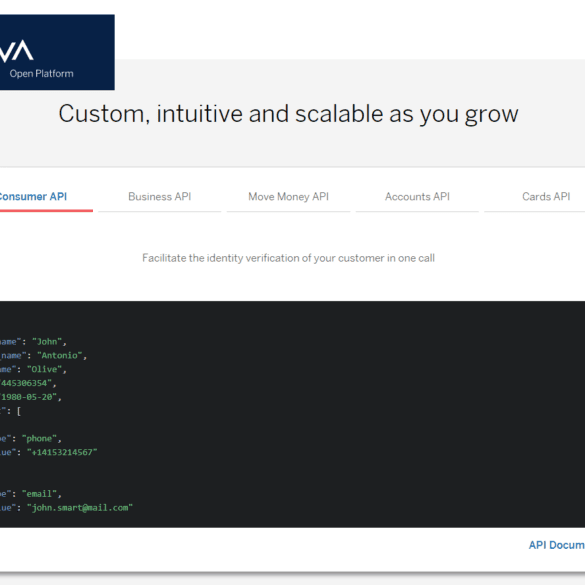

Anyone watching Fintech over the last decade has recognized an increasing shift of power from product manufacturers to the platforms where those products are sold. In the case of Amazon, Google, and Facebook -- finance is just a feature among thousands of others. I've made this point since 2017, when Amazon launched lending into its platform. Brett King has been a bit more generous in the categorization, calling the shift "embedded banking". This means that banking products are built into you life's journey, not accessed in a separate customer center location. The financial API trend is a tangible symptom of this vector.

This week’s PeerIQ Industry Update covers the great jobs report as nonfarm payrolls rose by 313,000 in February which caused the Nasdaq to hit an all-time high; CommonBond saw their first AAA rating by Moody’s and KBRA rated the senior bonds for OneMain’s latest deal at AAA, AA and A; PeerIQ also took a deep dive into the recent Amazon checking account news; they cover the benefits of the partnership, the significance of the deal and who might be next to enter the space. Source.

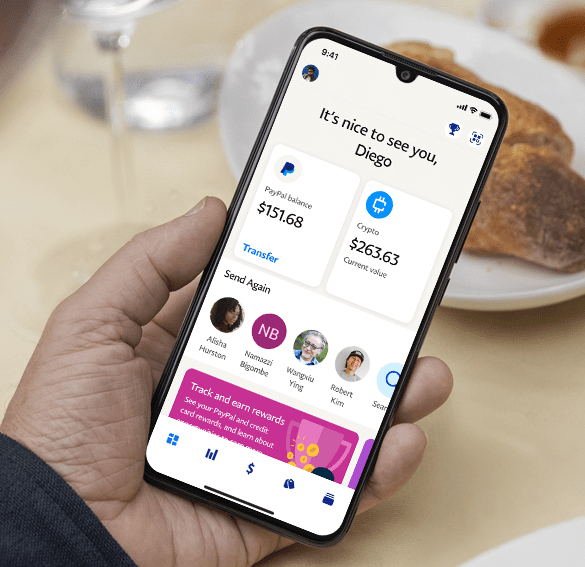

PayPal just launched what it calls a super app. It has a cash account with a 0.40% interest rate, direct deposit, money movement, bill pay, and remittance features. It also integrates shopping functionality with rewards and cash back. In this analysis, we compare this offering with Google Pay and Square Cash App, as well as trace the DNA of PayPal to understand whether such an offering will succeed where others failed.

Much has been written about Amazon’s foray into financial services; a new survey shows that 3 in 10 consumers say...

The continued push by Amazon into financial services could have a bigger effect on startups over banks; Nicolas Parmaksizian, global head of Capco digital, tells TearSheet, “If you combine an Amazon with a Capital One, you’re combining the amazing power of Amazon and Capital One’s data analytics, and that’s a challenging thing to compete with as a startup banking brand.”; digital only banks look to offer a better experience at a lower cost than the traditional banks, adding Amazon into the mix could drown out those startups before they ever get going. Source.

Finance is everywhere, and everywhere is finance. Smart city supply chains, self driving car insurance, video game real estate markets -- no matter which frontier technology you touch, it will have embedded implications on the delivery of financial services. And why wouldn't it? Like the use of language, finance is a human technology that allows societies to coalesce and compete with one another (in the Yuval Harari sense). It lifts people out of poverty and into entrepreneurship through microloans, providing generational sustenance for their families. And of course it also throws them into pits of corruption and greed, as they drink too deeply from the rivers of securitization and political power.

But enough poetry! I want to talk about augmented reality, attention platforms, and the re-formulation of payments and lending propositions in a global context.

Maria Renz spent more than 20 years at Amazon and is now joining SoFi; Renz was most recently vice president...

Crypto isn’t magic. It’s math. Two trillion dollars worth of math.

We are still, often, asked incorrect questions about the crypto currency markets. Questions like — “but what is the fundamental value?”

You have to unpack the word “fundamental”. That word signals a Warren Buffet view of the world: there are companies out there, they have equity shares well specified by corporate law in a particular jurisdiction, some are expensive while some are cheap, and that bargain shopping can be determined by a spreadsheet analysis of their cashflows relative to others. It’s so fundamental!

The story of such fundamental truth is anchored in our cultural and social history. We can point to the intellectual tradition of rationalism and classical economics, and talk about the theory of the firm, and its production function. We can point to how these things grew out of governance by religion, and natural rights as granted by a deity, and all sorts of other non-empirical hand waving.