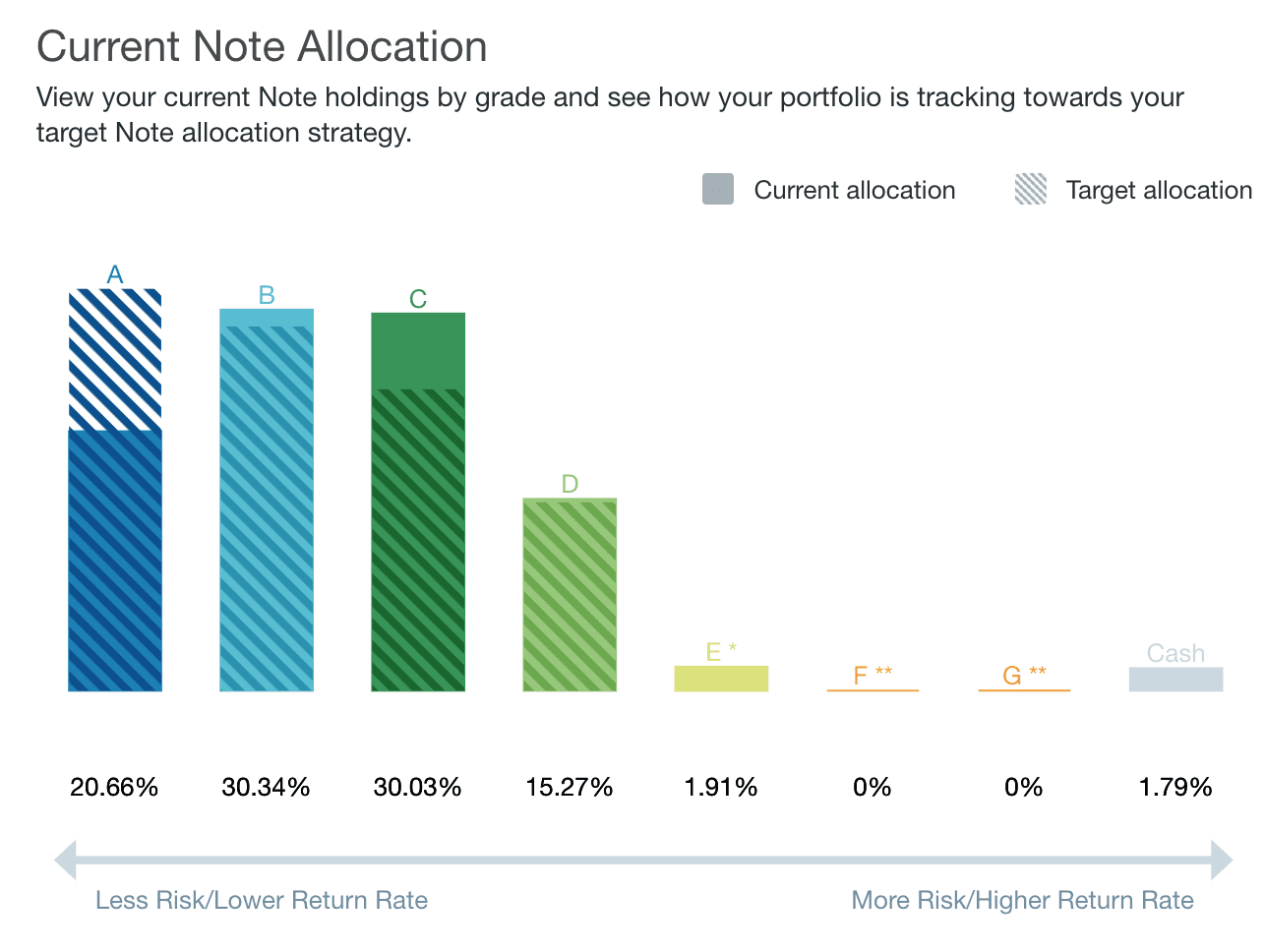

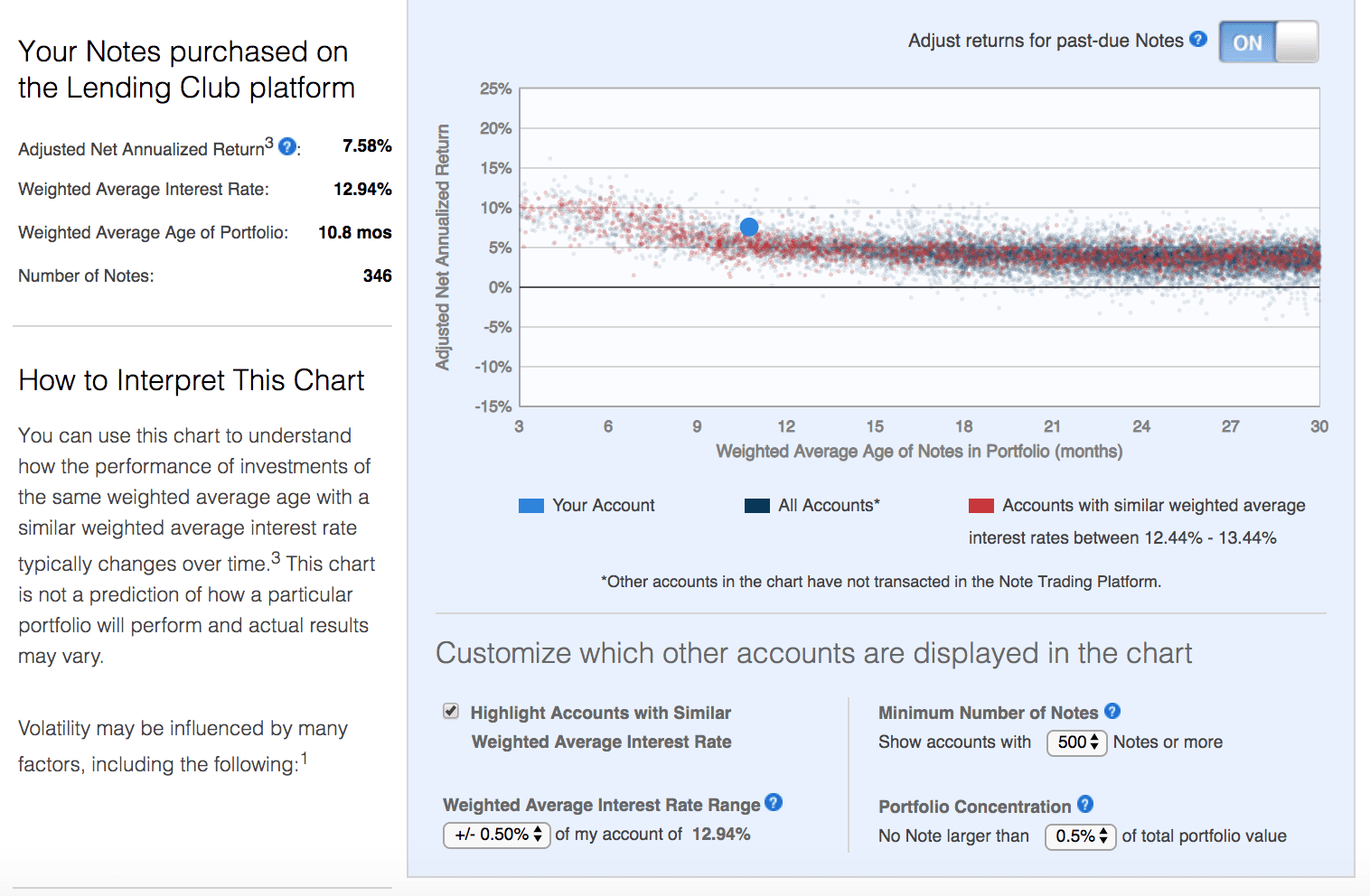

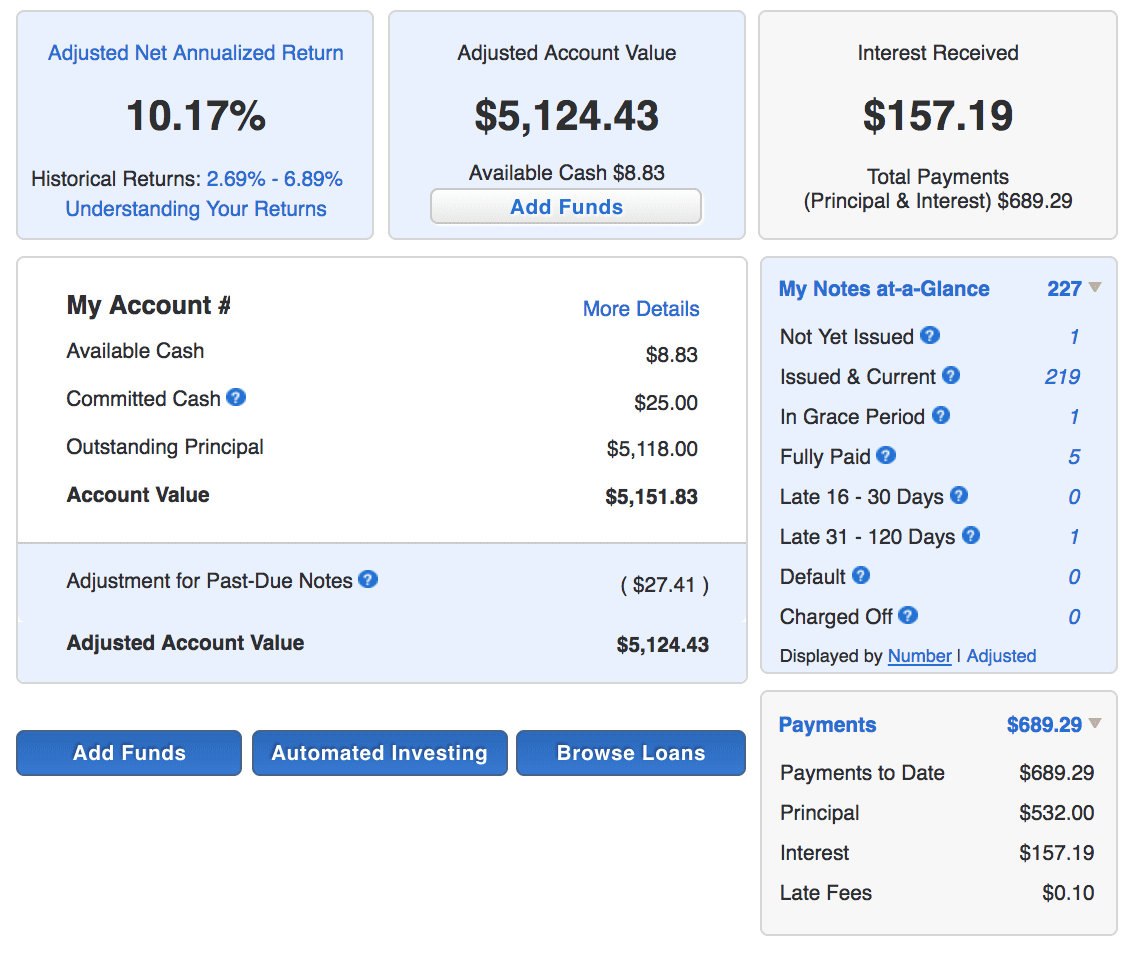

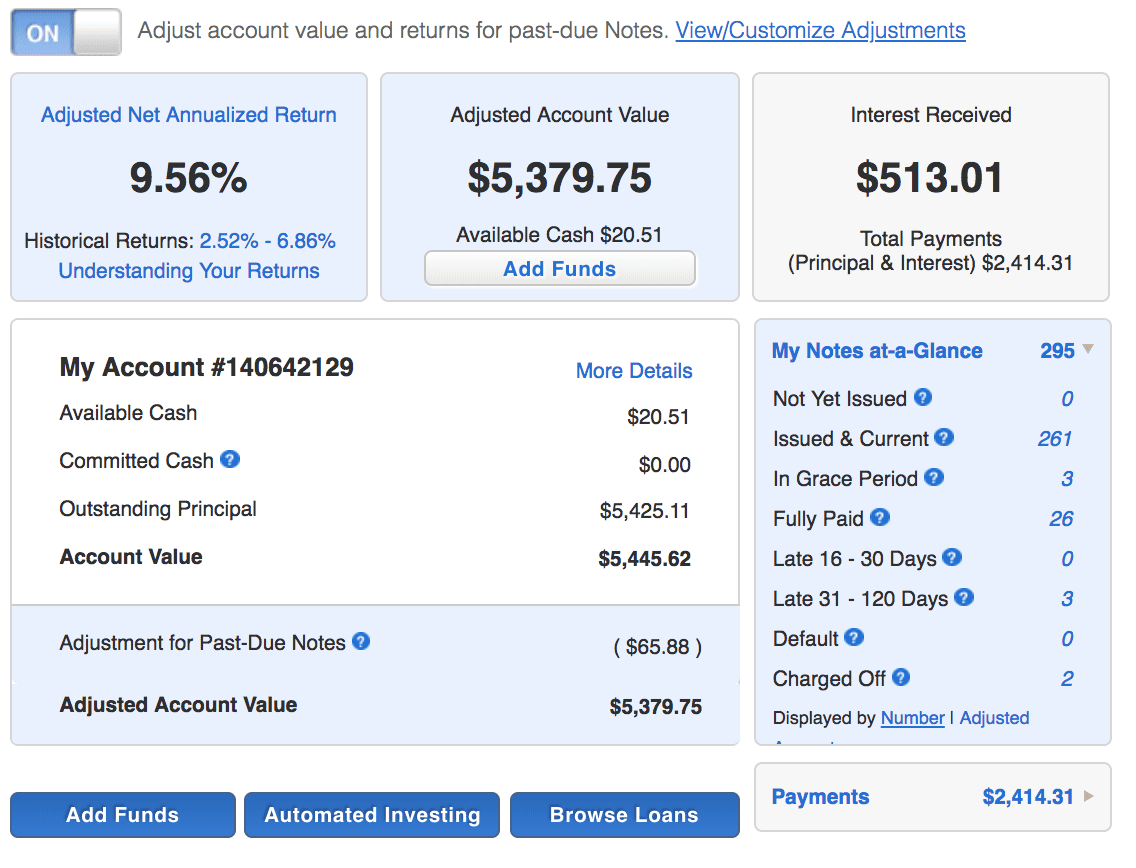

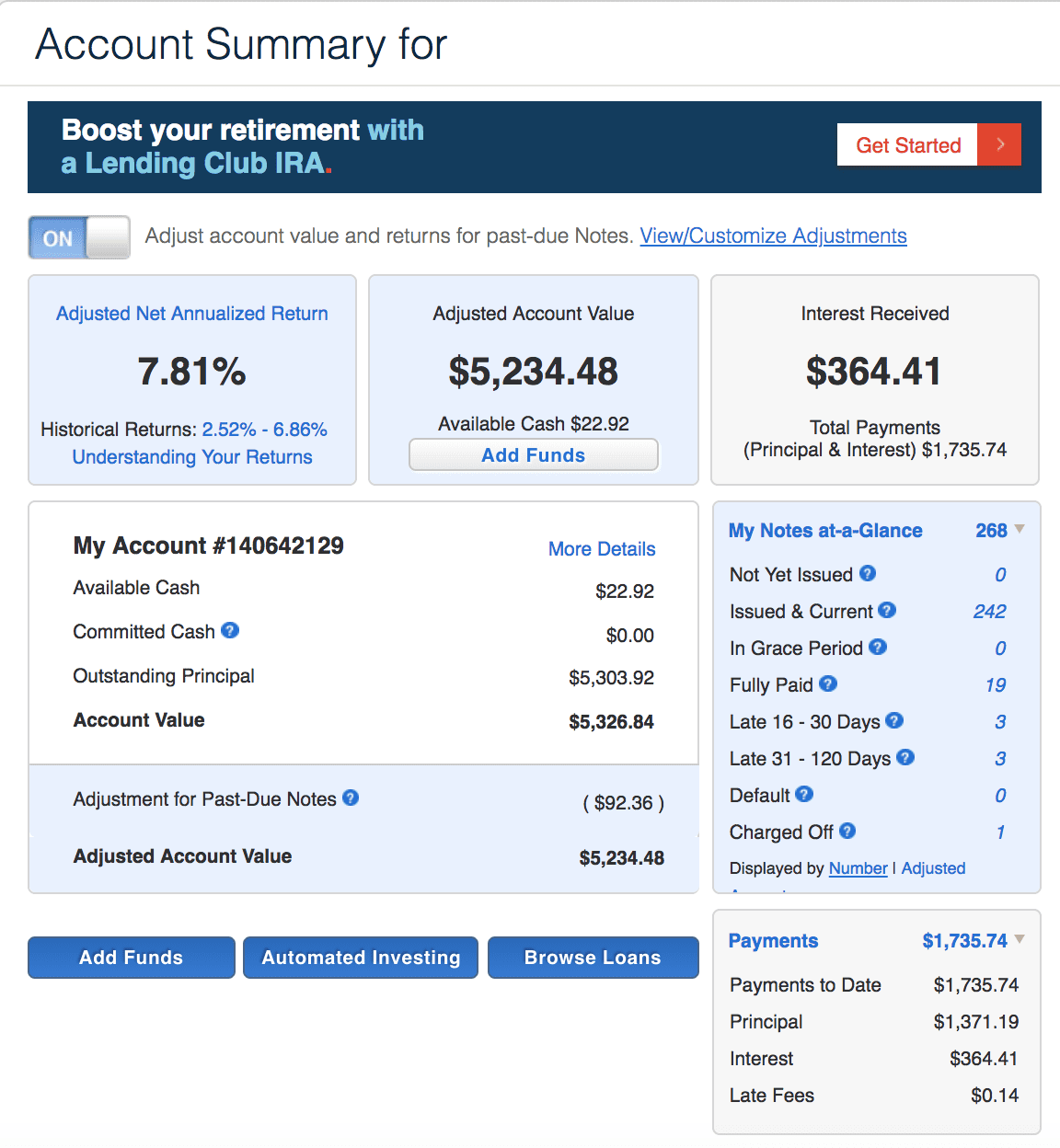

Peer to Peer Lending·Jul. 11, 2019New LendingClub Account Performance – Q2 2019In April 2018, LendingClub provided us with $5,000 to open a brand new account. Since then we have been chronicling the status... Read Full Story

Peer to Peer Lending·May. 14, 2019New LendingClub Account Performance – Q1 2019In April 2018, LendingClub provided us with $5,000 to open a brand new account. Since then we have been chronicling the status... Read Full Story

FintechNews RoundupUSA·Jan. 28, 2019Is SoFi Money the Bank Account of the Future?SoFi Money is one of the latest offerings in the digital banking space; SoFi is able to offer this checking/savings... Read Full Story

FintechNews RoundupUSA·Jan. 9, 2019Affirm to Pilot High-Yield Savings AccountsThe company is introducing the new account by leveraging a bank partner; the account will pay 2% APY and will... Read Full Story

Peer to Peer Lending·Jul. 12, 2018New LendingClub Account Performance – Q2 2018Back in April 2018 we shared that LendingClub had provided us with $5,000 to start a brand new LendingClub account.... Read Full Story

FintechNews RoundupUSA·May. 15, 2019New LendingClub Account Performance – Q1 2019In April 2018, LendingClub provided us with $5,000 to open a brand new account; since then we have been chronicling the... Read Full Story

EuropeFintechNews Roundup·Feb. 13, 2019RateSetter Sees Success with ISAIn just one year after launch RateSetter has brought in £175 million through their first ISA product; the cash invested... Read Full Story

Peer to Peer Lending·Jan. 23, 2019New LendingClub Account Performance – Q4 2018In April 2018, LendingClub provided us with $5,000 to open a brand new account. Since then we have been chronicling the status... Read Full Story

Peer to Peer Lending·Nov. 1, 2018New LendingClub Account Performance – Q3 2018In April 2018, LendingClub provided us with $5,000 to open a brand new account. Since then we have been chronicling... Read Full Story

FintechNews RoundupUSA·Apr. 6, 2018Lend Academy Article: How to Open Up a New LendingClub Account in 2018In this post we share the process of opening up a new LendingClub account, the first in a new series we will be sharing over the coming quarters. Source Read Full Story