When Renaud Laplanche started Upgrade in 2017 there were high expectations that the fintech pioneer would be breaking new ground with his second startup. After leading LendingClub from inception through IPO to the leading personal loan provider in the country everyone wondered what he had up his sleeve with Upgrade.

At his LendIt Fintech USA keynote in 2018 Renaud first teased us with his idea of the revolving personal line of credit. And he then confirmed earlier this year in his 2019 LendIt keynote that an Upgrade card was coming. Today is the day, the Upgrade Card has officially launched and it could be a game changer for the industry.

I caught up with Renaud earlier this week to discuss this new card and what it means for Upgrade and for the future of credit cards. He first pointed out that the concept of minimum monthly payment, that is a feature for most credit cards, is such a bad idea for consumers. It is detrimental to consumers’ financial health because it can take decades to pay off a credit card balance and result in a total payment often more than double the original amount.

He argues that this kind of credit card is fundamentally flawed and that a new approach is needed. He said:

I am genuinely more excited about this product than when I first launched online personal loans over a decade ago. We have refinanced tens of billions of dollars in credit card debt but still the overall outstanding balance keeps increasing. It feels good to get to the heart of the problem and create a more responsible card.

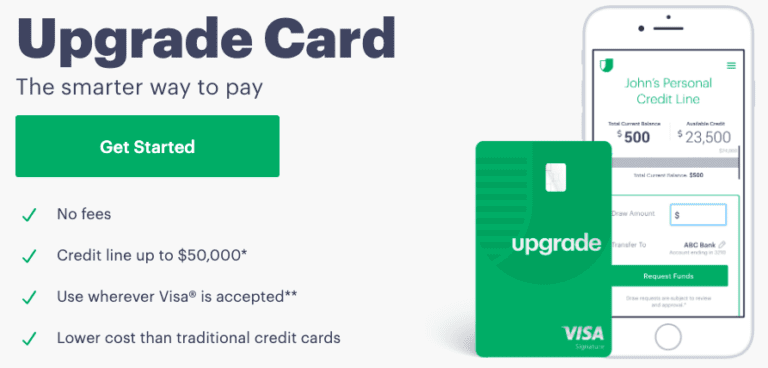

How Upgrade Card Works

You can think of Upgrade Card as a cross between a traditional credit card and an installment loan. Once they pass underwriting a customer is approved for a credit limit as you would expect. The difference is how the outstanding balance is paid back. Also, to be clear Upgrade is not calling this a credit card, it is simply Upgrade Card because they want to position it as a better alternative (an upgrade if you will) to a credit card.

Every month the new charges on the card are converted into an installment loan of either 12, 24 or 36 months duration (occasionally a 60 month option will be offered). The customer can choose their default payback period when they apply for the card and can actually change that duration for new charges at any time.

Each month the monthly payment due is calculated by adding up all the installment loan payments. But this is all done automatically for the consumer, all they see is the monthly payment amount that is due. It has been created to ensure simplicity but also transparency as the customer can drill down to see the details of each of their installment loans if they want.

Another big difference between Upgrade Card and traditional credit cards is the range of interest rates, specifically for lower risk consumers. Upgrade Card offers true risk-based pricing with a range of 6.49% to 29.99%, compared to cards targeted at prime consumers which usually start in the teens. For comparison the popular Sapphire Reserve card from Chase has an interest rate range of 18.99% to 25.99% and the new Apple Card is 12.74% to 23.74%.

When you apply for a card Upgrade does a credit pull on your credit report just like they would for a personal loan. Then they do a monitoring soft pull every month so they can reprice the credit line for any new balance if necessary. They also get push notifications from the credit bureaus during the month if any of their customers have a major event that might impact their credit, a very useful feature.

Upgrade Card balances will be funded by existing Upgrade investors. It is really a similar product to the existing installment loans from an investor perspective so they will see similar cash flows. Many like the ongoing credit monitoring and the ability to reprice risk on the fly.

There will be no origination fees so Upgrade will make money in two ways. First, there will be interchange revenue as with any credit card and second Upgrade will be selling these card receivables to investors at a premium.

The card has been offered in limited beta to Upgrade’s existing customers for the past three weeks and is available to everyone starting from today. The Visa cards are issued by Sutton Bank and the personal credit lines are issued by Cross River Bank. Cross River has a long history of innovation in the fintech space so it was not surprising that Upgrade chose them as the partner bank to issue this new kind of loan.

Renaud said this is the first card that is good for your financial health because it comes with the discipline of paying down your balance each month and not getting trapped in a revolving debt cycle like traditional credit cards, adding “Upgrade Card is the vegetable of the credit card world.”

My Take

Credit card debt is still a growing problem in this country. Ever since the financial crisis the total amount of outstanding credit card balances continues to increase. I am a big fan of a product that will encourage more responsible use of credit and Upgrade Card certainly has the potential to do just that.

Whether or not people will be happy to pay a higher monthly payment than they have been used to remains to be seen. But I think there is a good portion of the credit card population who do not want to carry a balance for decades, they genuinely want the forced discipline that an installment loan-type product demands.

In reality, this is how credit cards really should function. It should not be possible to take out a multi-decade loan for an everyday purchase. Upgrade Card is really creating the credit card as it should be. If this catches on it will be a real game changer for the industry.

People know they should eat their vegetables and those motivated to live a healthy lifestyle do just that. People also want to be more financially healthy. Upgrade is counting on those who are motivated to improve their financial health but still want the convenience and utility of a credit card. There are potentially many millions of people who fit that description.