Back in April at LendIt USA 2016, Lending Club teased that they would be announcing a new consumer lending product in June. This was pushed back following the subsequent news that rocked the marketplace lending industry. Now just a few months later Lending Club has officially announced their move into auto lending with a refinance product focused on prime consumers.

We spoke with Todd Denbo, Vice President of Consumer Auto Lending at Lending Club to learn more about the product and his experience prior to joining Lending Club. Todd has been with the company for a year and a half and his previous experience includes nearly 17 years at Wells Fargo. He worked in consumer lending on the credit card side and also led direct auto for a number of years at Wells Fargo.

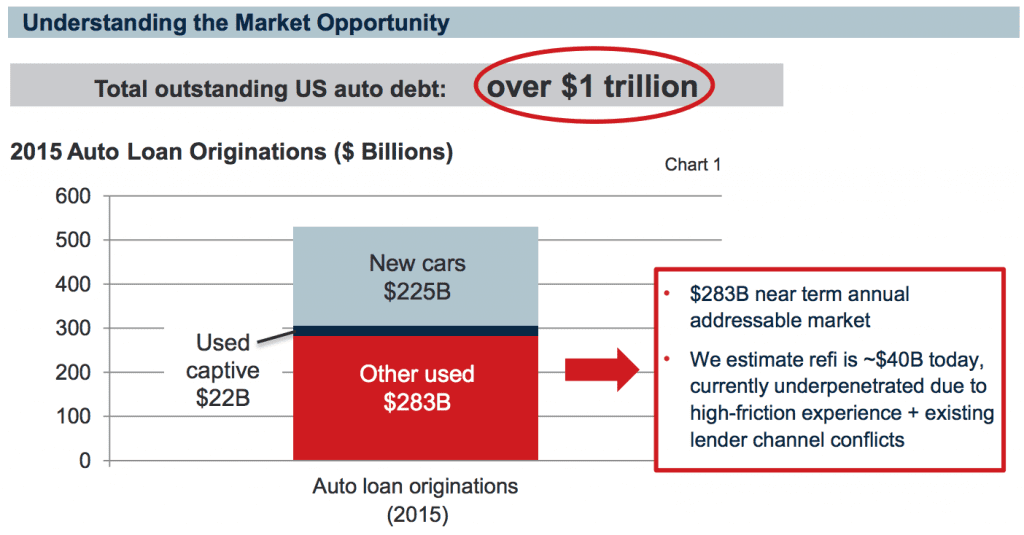

While the entire outstanding debt for auto loans totals $1 trillion, Lending Club estimates that the refinance market stands at $40 billion annually today. Todd believes the market opportunity for auto refinance is at least double that size if the process for obtaining a loan was more simple. The problem in the auto refinance space is that the process is cumbersome and consumers equate the pain of refinancing an auto loan to that of going through a mortgage refinance.

According to Todd, the major player in auto refinance is Capital One along with some banks and credit unions. Most banks don’t focus on refinancing auto loans since they have deep relationships with dealers who markup the loans. Since consumers usually negotiate on the price of a vehicle and fail to shop around for credit, consumers are paying more than they need to. According to Lending Club, consumers pay 200 bps higher interest rates than they should. This 200bps difference is $1,350 the consumer could otherwise be saving over the life of the loan.

The Lending Club Auto Refinance Product

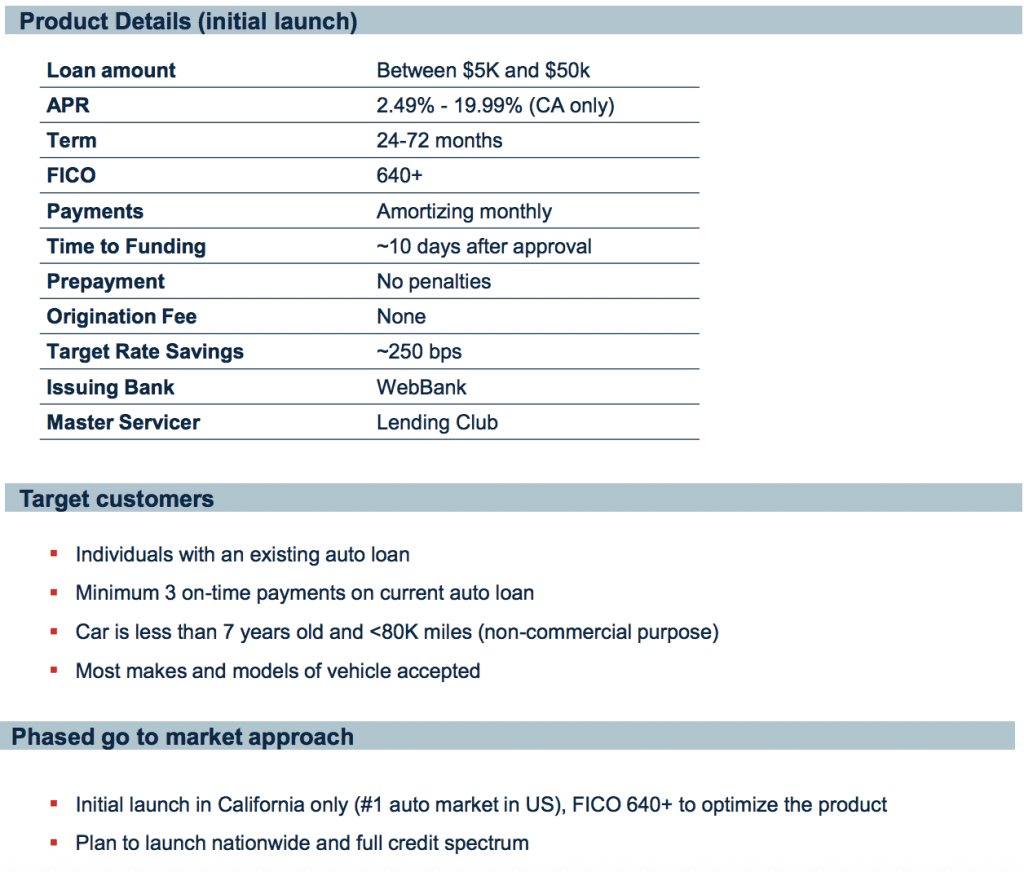

The new refinance product is initially only available to borrowers in California, but we can expect that they will roll this out similar to what they have done with their unsecured loan product over time. Lending Club will lean on the same marketing channels as their core unsecured product for customer acquisition. They plan to leverage data sources to target borrowers who have demonstrated on-time payments and help consumers by offering a more affordable loan. Below are the details of the initial offering to prime consumers:

Todd shared that the average loan on used cars is in the high single digits with an average loan size of $18,000. With rates starting at just 2.49%, Lending Club can provide significant cost savings to prime borrowers.

Offering a compelling product from a cost savings standpoint is only one piece of the puzzle. Lending Club also needs to deliver on speed and customer experience. Lending Club states that the speed to offer is on average less than 1 minute for borrowers to see what offers are available which includes loan rate and term. There is no impact to the borrower’s credit score. Borrowers will be given two offers, lowest APR and lowest monthly payment and the application process will look similar to that of their unsecured consumer loan product.

What’s most interesting is that Lending Club has significantly streamlined the application process compared to what currently exists in the market. Todd shared that on average most companies who currently offer auto loan refinancing will ask north of forty questions. Lending Club’s application will have a dozen questions about the individual and five questions about the vehicle. Lending Club has also moved questions about the VIN number and getting in touch with the previous lender about the previous loan amount to the end of the loan process.

Besides underwriting just the consumer, Lending Club will plug into data sources from TransUnion and NADA to determine a vehicle’s value. They are also leveraging a leading loan servicing company in the auto segment. According to Todd, servicing auto loans is a critical part of the equation and they wanted to use an industry leader. Todd stressed that this is a conservative step into auto, focusing on the prime consumer and that the goal is to keep the consumer in the car as long as possible. In the event that a consumer fails to pay, the third party servicing company will repossess the car.

Auto Lending Historical Performance and Loan Funding

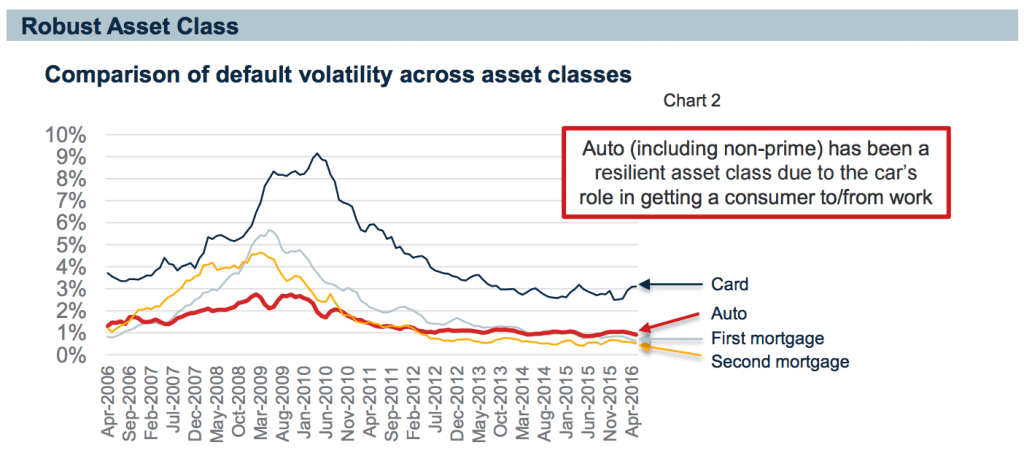

Lending Club also shared historical defaults across various asset classes since early 2006. Looking at the chart below, the auto lending vertical is a relatively stable performing asset class even in the depths of the recession compared to mortgages and credit cards. Since mid 2011, defaults in auto lending have been extremely stable at around 1%.

As Lending Club CEO Scott Sanborn reiterated at last month’s Marketplace Lending + Investing event, Lending Club continues to focus on the pure marketplace model. However, Scott did mention that they do lend on balance sheet for new product launches and that is the plan with this new auto refinance product. Todd noted that they are already in talks with several institutional investors to invest in whole loans, similar to how institutions invest in Lending Club’s unsecured loans. Given that this is a brand new product, it will only be available to institutional investors. We will have to wait and see if Lending Club ever opens up access to the retail investor community.

Conclusion

When I first heard the news of Lending Club’s move into auto lending I was surprised that the launch had only been delayed 4 months. The summer of 2016 brought news of many companies scaling back and Avant publicly announced that they were delaying their own auto lending plans. Many people have doubted Lending Club in recent months and there has been no shortage of negative news stories on the company and on the industry. It’s great to see that Lending Club continues to push forward despite the headwinds of 2016. It seems that things have stabilized for Lending Club to a point that they were comfortable in expanding to a new category.

Entering into auto refinance is a different beast than unsecured loans, but is a natural expansion for a company that has had incredible success in consumer lending. The biggest challenge that Lending Club may have is making consumers aware of auto refinancing as it is not a commonly discussed product compared to mortgage refinance. It will be fascinating to watch and see if they can bring their successes in unsecured loans to the auto space.