Lending Club held its first earnings call announcing Q4 2014 earnings results. The stock has had incredible swings since the original IPO price of $15. The stock opened 56% higher on its debut and eventually reached a high of $29.29, only to eventually fall to a low of $18.30. It closed today at $23.65 before earnings.

Since going public, Lending Club has been anything but quiet, announcing a Google partnership, a deal with Alibaba and finally a deal with 200 community banks.

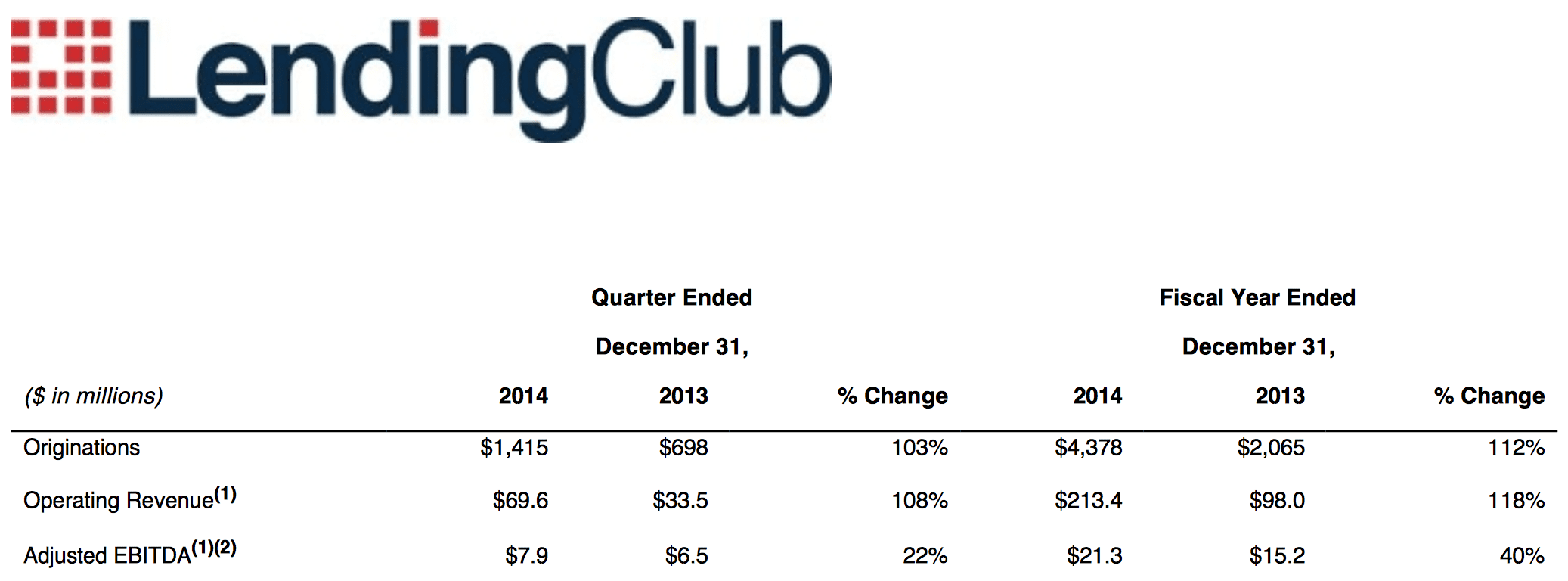

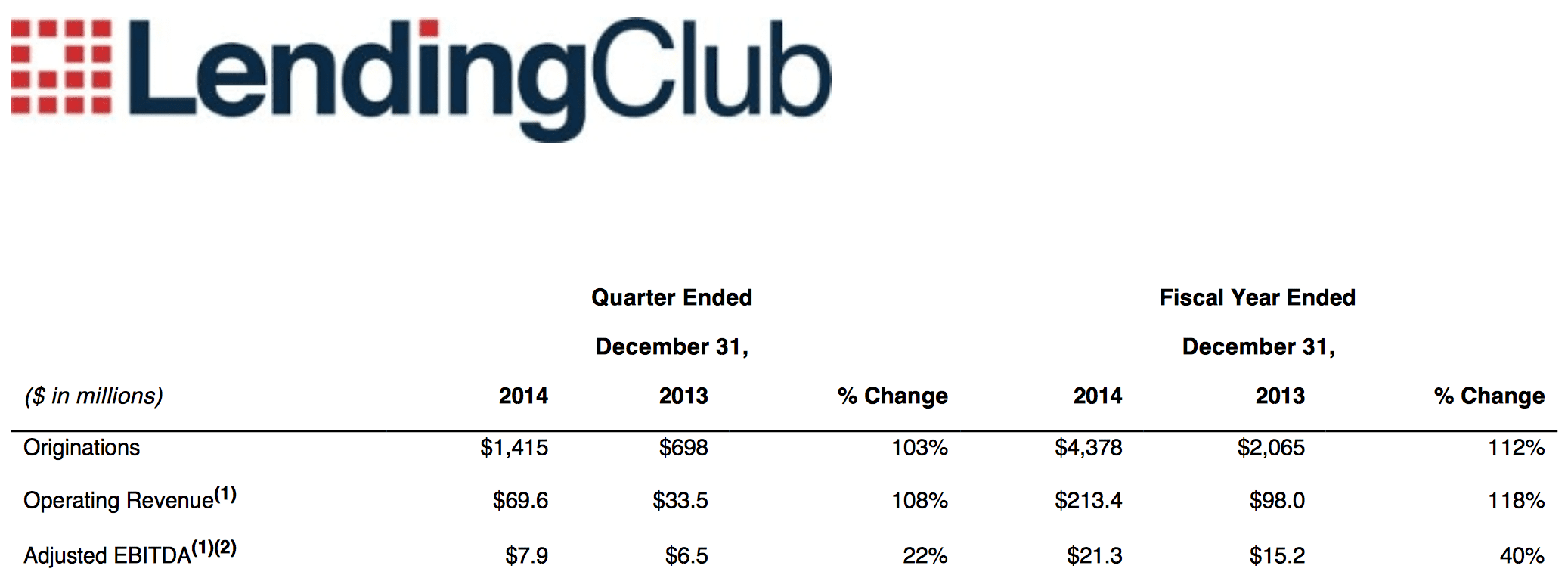

Beating analysts predictions, Lending Club announced Q4 2014 revenue of $69.6 million and an adjusted EPS of .01. An average of revenue estimates were projected to be $66.67 million with an EPS of .01. Lending Club originated $1.415 billion worth of loans, compared to $698 million last year. This is an increase of 103% year-over-year. Q3 originations were $1.165 billion, which shows Lending Club’s consistent origination growth we’ve been accustomed to seeing.

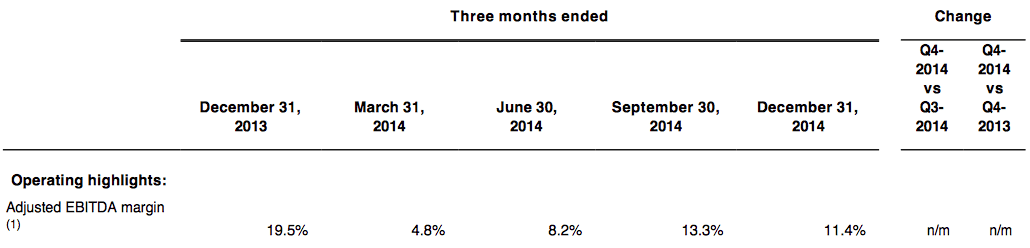

The theme of this earnings call is that they are investing heavily in the company. They have solid EBITDA margins, but Renaud stated that long term margins could reach 40%. Below shows their EBITDA margins over time.

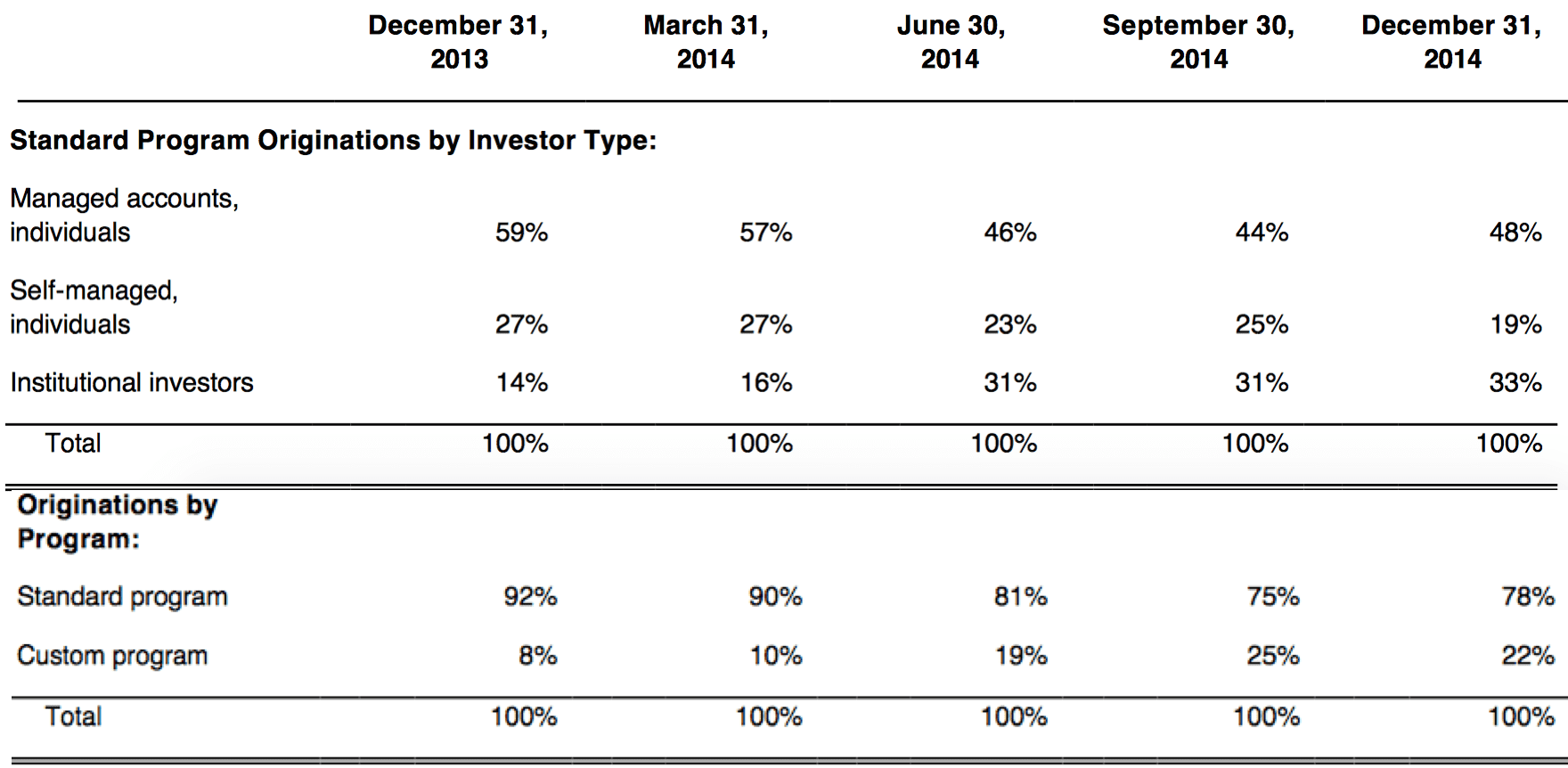

Lending Club provided the below information regarding the standard program originations by investor type and originations by program. I believe institutional investors are being under represented since standard program originations don’t include investors in the custom program loans. These loans are not available directly on the marketplace. Custom program loans make up 22% of the loan volume as of December 31, 2014 and would include products such as small business loans, medical loans and their super-prime loans.

Renaud Laplanche said the following regarding the quarter:

“We have continued to expand our reach through 2014 by doubling the size of the business again, while continuing to invest heavily in future growth and risk management,” said Renaud Laplanche, CEO and founder of Lending Club. “Our IPO in December was an important milestone in the life of the company, and everyone at Lending Club is excited about the next 5 to 10 years and committed to delivering more value and a great experience to our customers. 2015 is going to be another investment year, and we intend to continue growing originations and revenue at a fast, yet deliberate pace.”

Looking forward to Q1 2015, LendingClub expects $74 to $76 million in operating revenues and an adjusted EBITDA between $6 and $9 million. The outlook for total revenues for 2015 is expected between $370 million to $380 million and an adjusted EBITDA between $33 and $42 million.

There were several questions that were asked and I’ll highlight a few takeaways below:

- They are investing heavily in people with an aggressive hiring plan. The increased brand recognition with the IPO has aided in acquiring top talent. They have almost doubled their headcount since Q4-2013.

- Regarding the new partnerships, two of which are in small business lending, they are looking to leverage the data to help with underwriting loans. They expect low acquisition cost for these borrowers and passing on cost savings to the customer.

- Lending Club’s strategy will continue to be focused on the US market since there is such a large opportunity, both with existing and new products. They believe there is no urgency to exploring other markets at this point in time. They plan to take more of a wait and see approach to see how new platforms perform internationally until they jump in. There are certain unknowns when it comes to expanding internationally, such as regulation. Should they decide to expand internationality, the entry point may be higher, but Renaud viewed this as less risky.

- Institutional and retail demand continues to be high and they like each type of investor for different reasons. Institutional investors are able to scale and retail investors will likely stay around for the long term. Renaud mentioned that there are lots of individuals investing in retirement accounts.

- There has been no loss in efficiency in terms of marketing expenses and loan acquisition costs for their core product. If anything, efficiency has been increasing. Reputation building has helped to convert new borrowers and existing customers are great product ambassadors for Lending Club. In terms of interest rates, investors perception of the risk is coming down and in turn, they are willing to accept a lower return. This has helped on the borrower side as they can offer even better rates to fuel growth.

- Despite interest rate declines, investors are still showing an appetite for their loans. However, they continue to monitor this as interest rates change.

This was a solid first earnings report for Lending Club as a public company. Earnings were in line with expectations and revenue beat expectations. Loan origination growth was solid, still maintaining the rapid growth that has been the industry’s hallmark. Renaud Laplanche ended with stating that they truly believe they are only getting started.

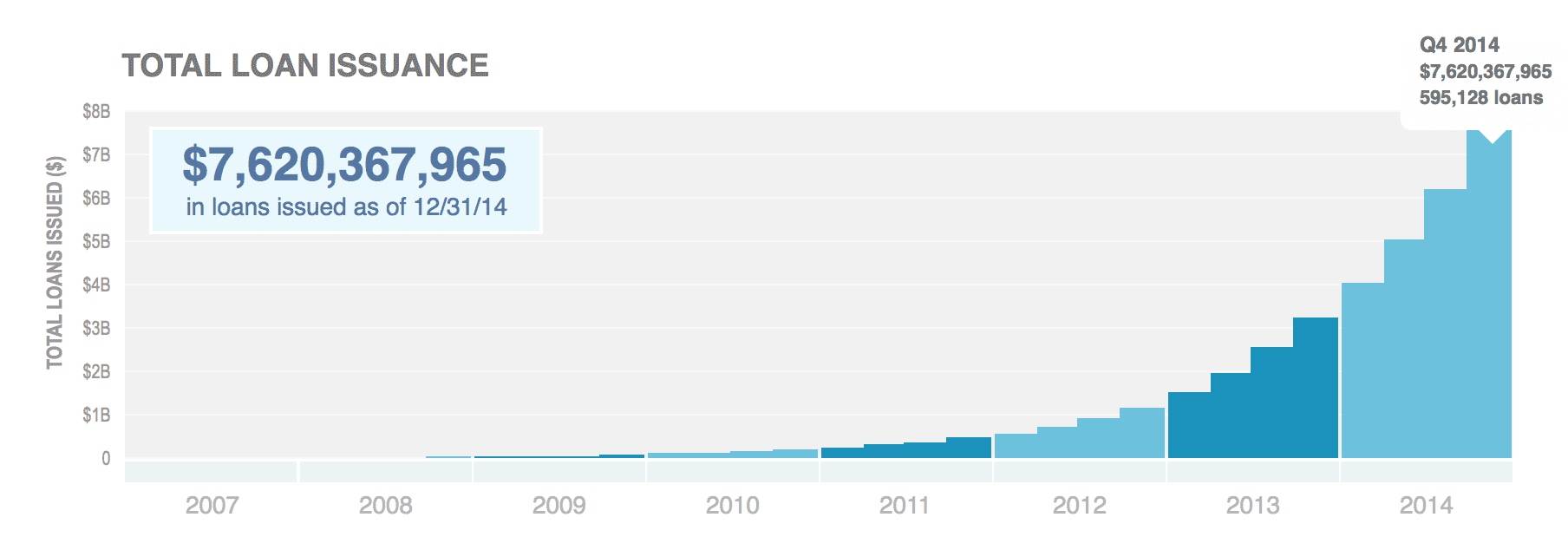

Many investors will be happy to know that they can download the most recent loan data from Lending Club’s statistics page.

At time of writing, the stock is down around 11% at $21.10 in afterhours trading.

I welcome any discussion on Lending Club’s first earnings report in the comments.