Last Friday Peter and I had the honor of joining the CreditEase team on the NYSE floor to ring the opening bell and celebrate the successful initial public offering of Yirendai, their online platform. It was an exciting moment for the company and our industry since it marks the first major IPO of a Chinese P2P company.

Last Friday Peter and I had the honor of joining the CreditEase team on the NYSE floor to ring the opening bell and celebrate the successful initial public offering of Yirendai, their online platform. It was an exciting moment for the company and our industry since it marks the first major IPO of a Chinese P2P company.

Yirendai successfully raised $86 million by selling 8.6m shares at $10 per share and it closed the day at $9.10 for a market cap of $544 million (they have 58.5 million fully diluted shares outstanding). The stock trades under the symbol YRD and the IPO was led by Morgan Stanley and Credit Suisse.

Yirendai Spins out of CreditEase, the Largest P2P Firm in the World

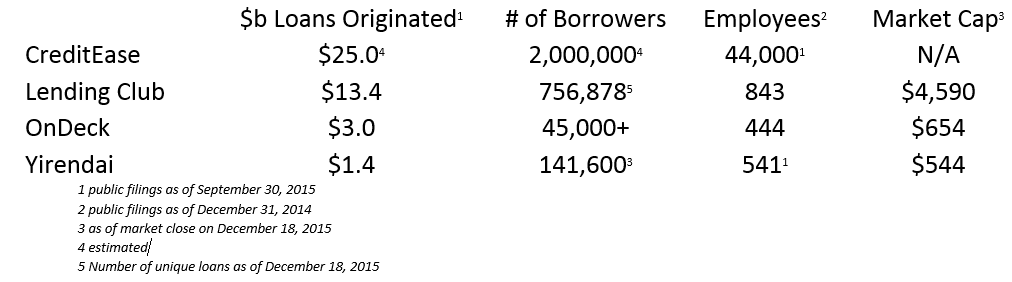

CreditEase is an enormous P2P company based in China. It was one of the first P2P companies in the world when it launched in 2006 and has evolved into a full service financial services firm that provides inclusive finance and wealth management products and services in China. We love analyzing CreditEase because they represent the future of P2P lending. Their focus on “inclusive finance” means that they offer products to borrowers across the credit spectrum ranging from prime quality borrowers, to near prime borrowers, to sub-prime borrowers.

Their first loan was a student loan and over time they have expanded to almost every major (P2P) lending category including student loans, auto loans, rural loans, mortgages, small business loans, and consumer loans for home improvement, weddings, vacations, and other life events. In addition, early on they realized that P2P lending was only their first product and they have since expanded to wealth management products, which include equities, real estate, credit, alternative investments, and insurance. They have a huge network of over 230 physical locations, they have grown to over 44,000 employees, and they have originated over $25 billion in loans. They are like Lending Club, Avant, LendUp, SoFi, LendingHome, and Charles Schwab wrapped into one company.

Let’s put it into perspective:

As you can see, the scale of CreditEase is much larger than most people in our industry realize. They have carved out Yirendai, which is their pure play online unsecured prime quality consumer lending platform that looks very similar to Lending Club or Prosper.

How Yirendai Works

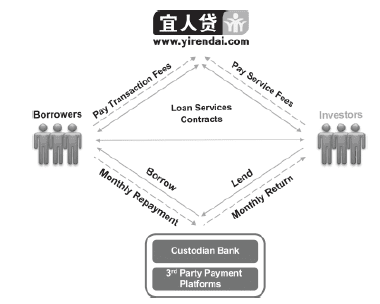

Yirendai is a consumer lending platform that connects borrowers with lenders and collects a transaction fee from the borrower and service fee from the investor, very similar to a standard P2P lending platform.

This is what their webpage looks like (notice that they are upselling their risk reserve fund, which they call portfolio insurance):

Here are some stats on Yirendai – notice that the average borrower borrows $9,989 per loan ($1.38b/141,600) and the average lender lends about $8,000 per loan ($1.38b/185,704) or ~80% of the loan, which seems high and suggests wealthy investors.

Four Key Topics: Mobile, Borrower Acquisition Costs, Reserve Funds, Grade D Loans

I see four key topics related to Yirendai.

Mobile is Important and Yirendai is Doing Well in Mobile:

Yirendai has facilitated $261m in loans through their mobile applications through 3Q15, which has represented 26.5% of their total loan volume. They break out the total number of employees dedicated to mobile, which is 113 or 21% of their total staff (separate from their technology staff). I have personally seen and used their mobile application and I can tell you that it is a simple user experience and it is compelling for investors to easily invest through their auto investment offering to generate a 10-12% return. While the US has barely scratched the surface of mobile lending, in China having a mobile strategy is must have and a major key to success. We can learn a lot about mobile lending from the Chinese.

Borrower Acquisition Costs are Too High – They Need to Diversify Away from CreditEase:

Yirendai has been reliant on CreditEase as a borrower acquisition channel, with approximately 2/3 of its 98k borrowers coming from CreditEase referrals, which represents about 50% in terms of number of borrowers:

[table id=2 /]

* through September 30, 2015

Approximately 68% of those loans are originated from offline CreditEase channels through their branch network. Interestingly, CreditEase charges Yirendai 5% for each borrower referral and will increase to 6% for 3 years starting in 2016, which is about market rate in China. My sense is that Yirendai will diversify away from CreditEase and will likely continue to build their online channel. To put it in perspective, Lending Club probably pays at max $500 per borrower (likely much less) for a $12,000 loan or about 4.2%.

The Reserve Fund Makes a Lot of Sense and is A Model for Best Practices:

We believe that Yirendai is making a step in the right direction with their reserve fund. The average investor is China is unsophisticated when it comes to investing and does not have a firm grasp on the concept of risk/reward. Culturally, most investors seek high returns that are guaranteed (reward without the risk), so the P2P industry model was originally based on guaranteed loans. They would originate a high interest rate loan, offer a much lower percentage to the investor guaranteed, and make money on the spread. However, this form of “credit enhancement” created perverse incentives for the platforms to continue to originate riskier loans to capture higher spreads. Yirendai used a guarantee model from August 2013 to December 2014 then switched to a much more palatable reserve fund.

Under their risk reserve fund arrangement, if a loan is delinquent for a certain period of time, Yirendai may withdraw a sum from the risk reserve fund to repay investors the principal and accrued interest for the defaulted loan until the risk reserve fund is depleted. This is a pass through fund, which eliminates the incentive to capture spread/originate riskier loans. However, the fund is still finding its footing and changes are on the way.

For the past year Yirendai has funded the pool by taking 6% of origination fees but defaults are trending towards 7% so the management team will change their reserve to 7%.

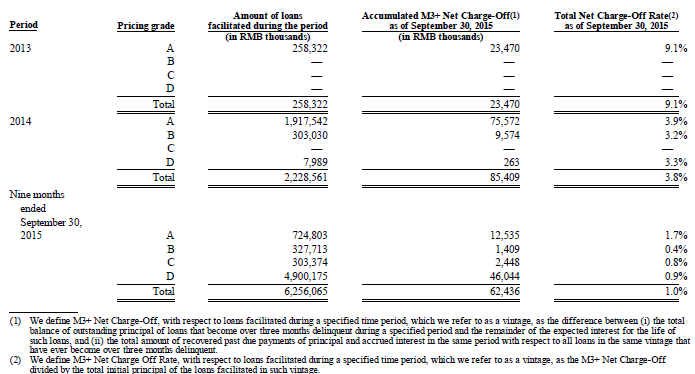

Grade D Loans are a Major New (Unproven) Initiative:

Yirendai launched Grade D loans in late 2014 and has since shifted the vast majority of their originations to this new grade. This is a result of risk based pricing. Yirendai originally offered one single product (Grade A) but has expanded its offerings over 2014 and 2015. So far in 2015 more than 77% of loans have been Grade D. We need to keep a close eye on these loans, which have a short credit history on Yirendai, although they have a longer history on CreditEase.

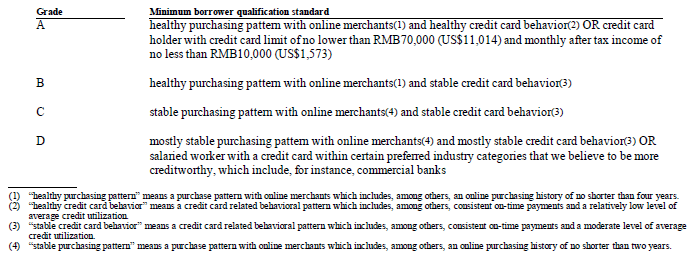

When I talked to the management team they told me that they are getting more sophisticated with risk based pricing and many of the borrowers that are now graded as D grade would have previously been graded B or C. Here is how they define their grades:

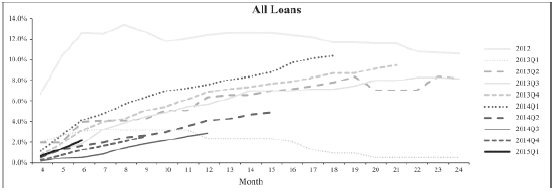

While it is still early, the 1Q15 vintage, which is the first vintage made up mostly of Grade D loans, is performing in line with previous vintages, which is a positive surprise since it really should trend towards higher defaults. If they keep defaults down then the benefit will be passed along to investors, which will generate returns higher than the 10-12.5% targets.

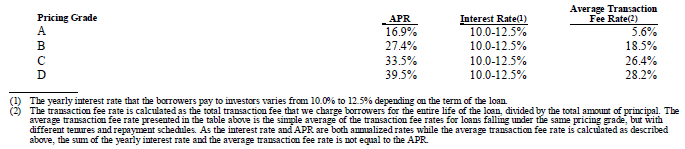

The economics on Grade D loans are amazing. Take a look at the transaction fees charged for Grade D loans: Yirendai takes a 28.2% transaction fee and charges a 39.5% APR to the borrower. Don’t forget that banks do not loan to consumers, so Yirendai, like most P2P lenders in China, is filling a gap in the market. Expect APRs to trend down as access to capital becomes more prevalent and credit underwriting standards strengthen.

Ok But What About Fraud, Lack of Regulation, and All of Those Failing Platforms in China?

Depending on whom you listen to, there are somewhere between 2,000 and 4,000 P2P platforms operating in China and if you listen to the media, they sensationalize the number of P2P platforms failures that occur. I consider the failures a non-issue since a vibrant start-up community should have many successes and failures. The more important issues are fraud and regulation.

Yirendai is Able to Use Fraud Detection as a Competitive Advantage

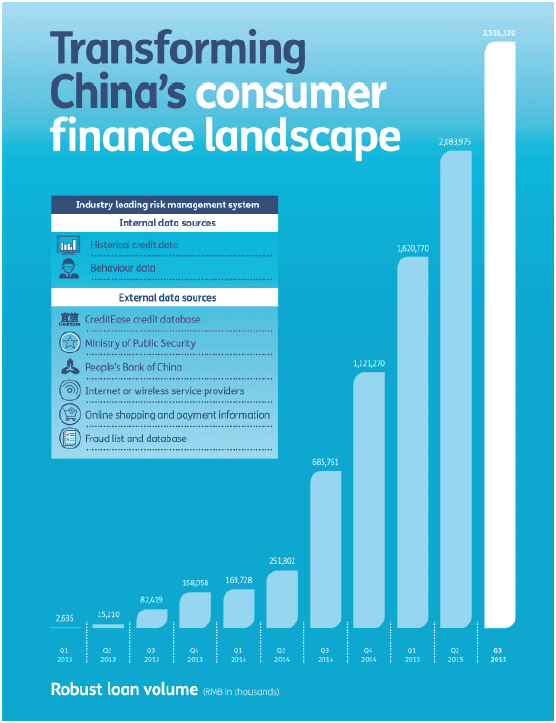

The national credit bureau in China covers only 300 million people out of their 1.6 billion population or about 18% of the population. This is a major issue for P2P platforms that must assess the credit worthiness of people with little verifiable credit history. Yirendai has a nice advantage over its competitors since its parent company, CreditEase, has a huge base of 2 million borrowers to draw data from. Their risk management system has 9 years of data and continues to strengthen over time as they continue to add new borrowers and new data. Currently, the company creates a “Yirendai Score” for every prospective borrower that is based on over 1 million pieces of data.

Regulation Is Coming and That is A Good Thing:

The Chinese P2P market is currently unregulated and has many instances of fraud committed by both borrowers and platforms. However, the market is huge with a cluster of large industry leaders and a long tail of small emerging companies. The industry leaders, like CreditEase/Yirendai, are setting an example for the rest of the industry. CreditEase is actively involved with government regulators to support the development of an industry framework. The government has been very involved in researching the Chinese market as well as global markets for best practices to include in their regulation. Over the past few years, our team at LendIt has brought global industry associations and regulators like the P2PFA and the International Organization of Securities Commissions to China to meet with CreditEase and with government regulators about policy development.

Here is the current state of regulation taken from Yirendai’s public filings:

On July 18, 2015 the People’s Bank of China together with none other PRC regulatory agencies jointly issued a series of policy measures applicable to the online peer-to-peer lending service industry titled the Guidelines on Promoting the Healthy Development of Internet Finance, or the Guidelines. The Guidelines introduced formally for the first time the regulatory framework and basic principles for administering the peer-to-peer lending services industry in China.

The Guidelines specify that the China Banking Regulatory Commission, or the CBRC, will have primary regulatory responsibility for the online peer-to-peer lending service industry in China and that the online peer-to-peer lending services providers should operate as information intermediaries and are prohibited from engaging in illegal fund-raising and providing “credit enhancement services,” which [Yirendai] believes are generally perceived in the online peer-to-peer lending industry to mean providing guarantees to investors in relation to the return of loan principal and interest.

A peer-to-peer lending service (i) is neither a credit intermediary bearing credit risk nor a transaction platform, but an information intermediary between lenders and borrowers, (ii) should not hold investors’ funds or set up any capital pools, and (iii) must not provide guarantees for lenders in relation to the loan principal and interest, or bear any system risk or liquidity risk.

Financial Performance Has Been Impressive

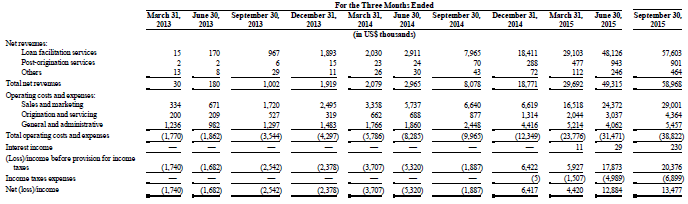

Yirendai is most definitely still a startup having operated for less than four years, however its growth is very impressive. In particular, 2015 has been a break-out year for Yirendai. I attribute the 2015 success to solidifying operations as well as the shift to the Grade D loans, which generate significant revenue for the company. As a result, Yirendai has reached profitability and is cash flow positive. While there are plenty of risks that I have outlined in this article, Yirendai is really well positioned for future growth in this large and exciting market in China. My final thought is that consumption in China is underfinanced primarily because loans from traditional financial institutions are not easily accessible. As P2P platforms like Yirendai proliferate, the consumption market is going to expand along with the platforms making the total addressable market an ever expanding market to serve. We expect Yirendai to continue to lead the way for P2P in China.

Further research available at Lend Academy and LendIt:

CreditEase Founder and CEO, Ning Tang, addresses LendIt:

State of the Union Address for the Chinese Internet Finance Market

Two articles about CreditEase from Lend Academy:

The World’s Largest P2P Lending Company That You Have Never Heard Of

Exclusive Interview with Mr. Huan Chen of CreditEase