Peer to Peer Lending·Sep. 23, 2022P2P payments growing as SMBs seek relief from high credit card fees: StudyBusiness.com's 2022 payment processing study reveals several marketplace disparities, beginning with credit cards and P2P payments. Read Full Story

AnnouncementsPeer to Peer Lending·May. 12, 2021LendingClub Chooses Alto as Their New IRA ProviderEric Satz soon realized there was a problem. The year was 2014 and he was trying to use his IRA... Read Full Story

Peer to Peer Lending·Jan. 26, 202112 Alternatives for LendingClub InvestorsIt has been almost four weeks since LendingClub closed down its retail investor platform and cash is already starting to... Read Full Story

Peer to Peer Lending·Oct. 7, 2020LendingClub Closing Down Their Platform for Retail InvestorsThere is big news out of LendingClub today for their tens of thousands of retail investors. They have given notice... Read Full Story

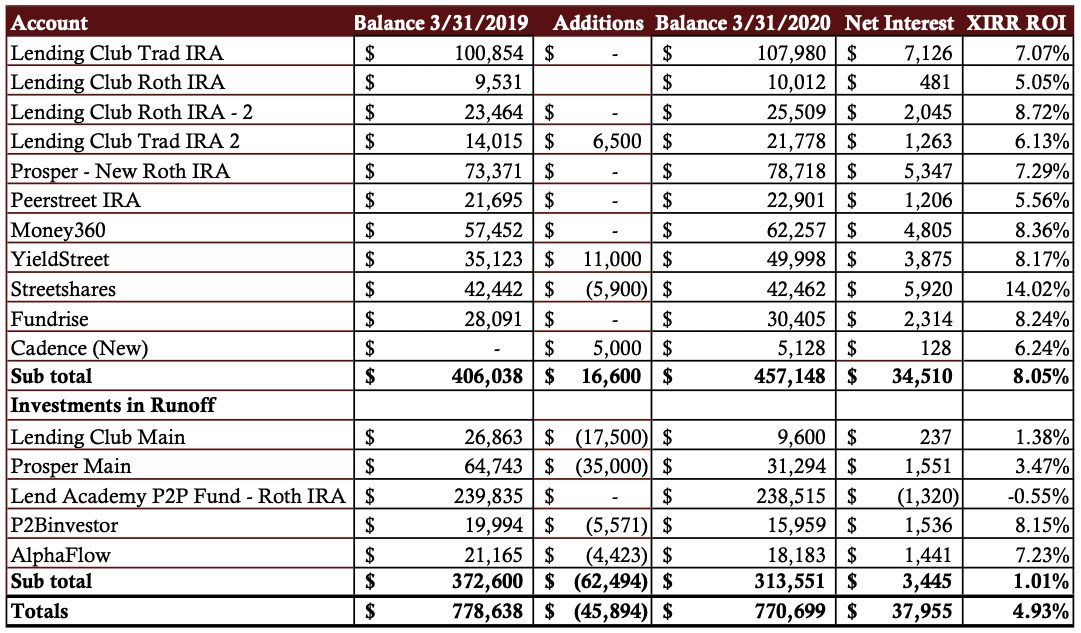

Peer to Peer Lending·Jul. 13, 2020My Quarterly Marketplace Lending Results – Q1 2020Many of you have emailed me to ask whether I am still doing these quarterly investment reports. The answer is... Read Full Story

Peer to Peer Lending·May. 28, 2020OnDeck Shares Early Progress in Borrower BehaviorThere has been a lot of uncertainty over the last 2 months, especially for fintech lenders. OnDeck found themselves in... Read Full Story

Peer to Peer Lending·May. 14, 2020Fintech Fundraising and M&A During a PandemicWhen it comes to fintech M&A and fundraising there is no better person to talk to than Steve McLaughlin. McLaughlin... Read Full Story

Peer to Peer Lending·May. 13, 2020Why Decentralized Lending Today is Like the Early Days of P2P Lending[Editor’s Note: In part one of this two-part series, Jason Jones, co-founder of LendIt and current CCO of Centrifuge, explains... Read Full Story

Peer to Peer Lending·May. 7, 2020Bernardo Martinez Steps Down as Managing Director Funding Circle USWe have recently learned that Bernardo Martinez is stepping down from his role as US Managing Director of Funding Circle.... Read Full Story

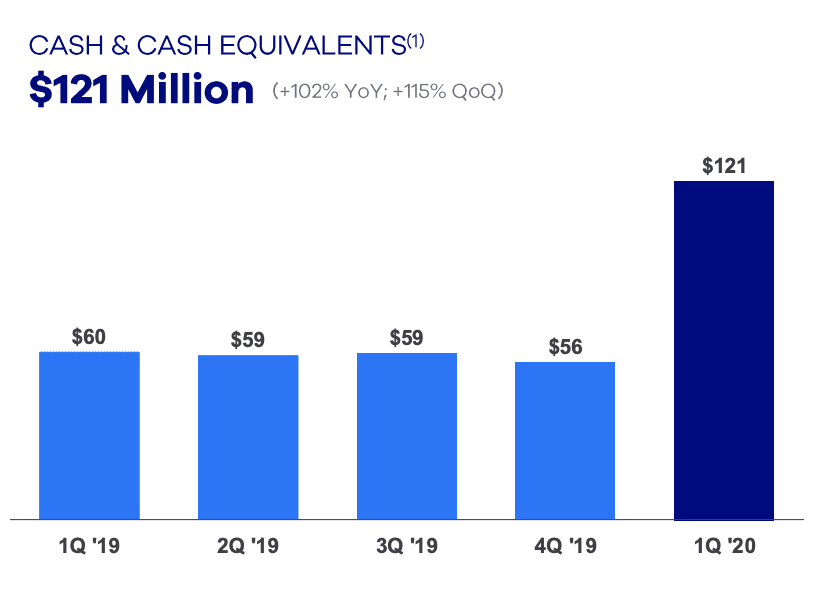

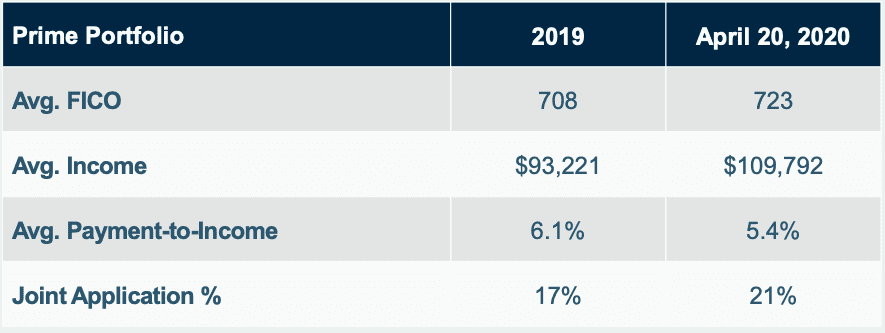

Peer to Peer Lending·May. 5, 2020LendingClub Releases Q1 2020 Earnings, Anticipates Originations to fall 90% in Q2Today LendingClub announced their Q1 2020 earnings. Lenders in the US are being hit hard by the coronavirus and we... Read Full Story